What is ecommerce bookkeeping? Learn how to handle online store finances

Mar 10, 2026

/

Larassatti D.

/

11 min Read

Ecommerce bookkeeping is the process of recording, organizing, and maintaining financial transactions for an online store.

Unlike traditional bookkeeping, online store bookkeeping handles transactions across multiple platforms, payment processors, and sales channels – making it more complex but essential for accurate financial management.

Effective ecommerce bookkeeping follows a five-step workflow:

- Recording sales from all channels

- Tracking both variable and fixed expenses

- Reconciling payments and payouts against bank deposits

- Managing inventory and calculating the cost of goods sold

- Generating financial reports

These steps transform raw transaction data into actionable insights about profitability, cash flow, and business health.

Daily bookkeeping tasks include recording sales and updating inventory levels. Weekly reconciliation confirms that payouts match sales records and catches discrepancies early. Monthly financial statements, such as profit and loss reports, balance sheets, and cash flow statements, provide a high-level view for strategic decision-making.

To make this workflow easier, specialized tools range from $15-30/month for basic bookkeeping software to $500-2,000+/month for full-service ecommerce accounting support.

The actual ecommerce bookkeeping cost will also depend on your transaction volume, number of sales channels, and whether you handle bookkeeping in-house or outsource to specialists.

Ecommerce bookkeeping explained

The definition of ecommerce bookkeeping centers on maintaining a company’s financial health through daily, weekly, and monthly tasks.

- Daily, ecommerce bookkeeping involves recording sales data from your online store, tracking refunds, and updating inventory levels as orders are fulfilled. This step ensures that revenue and stock movements are accurately reflected across your systems.

- On a weekly basis, bookkeeping includes reconciling payouts from payment processors, reviewing transaction fees, and confirming that deposits match your sales records. Regular reconciliation helps catch discrepancies early, before they snowball into larger financial issues.

- Monthly bookkeeping provides a high-level view of business performance. This includes generating financial statements, such as profit-and-loss statements and balance sheets, to understand trends and evaluate overall financial health.

Ecommerce bookkeeping also acts as the digital bridge between your sales platforms, payment processors, and business bank account. These systems don’t always sync perfectly, so a bookkeeper’s role is to ensure every sale, fee, refund, and payout is accurately reflected across all tools.

Ultimately, bookkeeping is a foundation of any successful online store, as it transforms raw data into a roadmap for business decisions.

For example, if shipping costs rise faster than revenue, accurate bookkeeping lets you adjust pricing or carrier choices before those costs threaten the long-term health of your business.

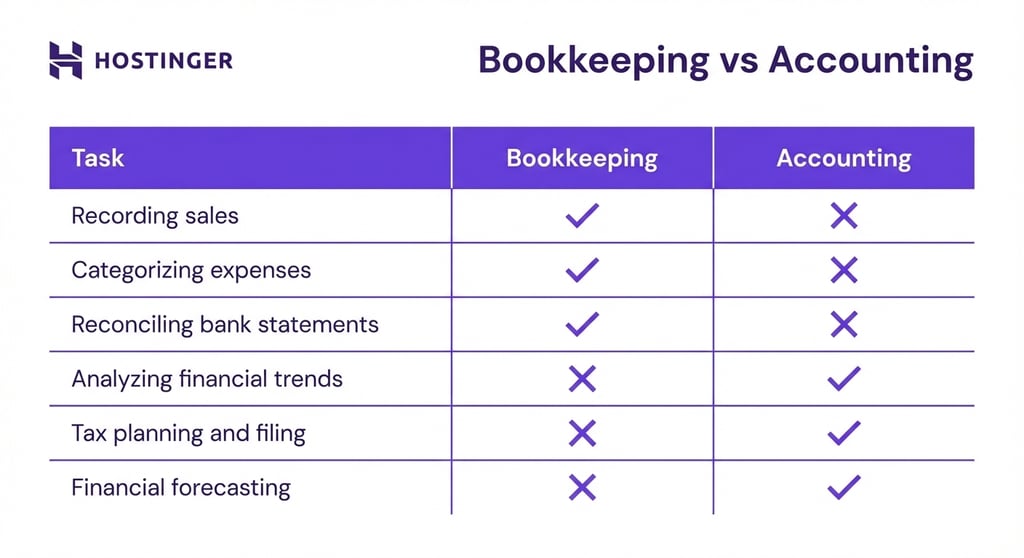

Ecommerce bookkeeping vs ecommerce accounting

The main difference between ecommerce bookkeeping and accounting is in how financial data is handled and used.

Bookkeeping forms the foundation of an online business’s financial system, which focuses on day-to-day administrative work.

Accounting builds on that foundation. It takes data from bookkeeping and analyzes it to generate financial reports, assess business performance, ensure tax compliance, and support strategic decision-making.

Every ecommerce business needs bookkeeping from day one. Even if you’re just starting an online store, you need consistent transaction tracking to:

- Monitor cash flow and profit margins

- Track sales, refunds, fees, and operating expenses

- Maintain accurate financial records

Without bookkeeping, it’ll be challenging to understand how the business is actually performing.

Meanwhile, accounting becomes essential as your ecommerce business grows in complexity. You’ll need an accountant when:

- Preparing and filing taxes or managing sales tax obligations

- Analyzing profitability across products, channels, or regions

- Planning for scaling, funding, or major investments

- Ensuring compliance with financial and regulatory requirements

In short, bookkeeping keeps your ecommerce business organized, while accounting helps you make informed decisions and stay compliant.

How ecommerce bookkeeping works

Online store bookkeeping follows a repeatable workflow that captures, categorizes, and verifies financial data across your store, payment processors, and bank accounts.

To make the process easier, you can use automation to pull sales, refunds, fees, and payouts into a central system and categorize transactions. Regular reconciliation confirms that records match actual deposits, keeping the books accurate.

When done consistently, this process creates reliable reports that reflect your business’s financial health and support better decision-making.

Step 1: Recording ecommerce sales

Recording sales starts with capturing every transaction across your ecommerce platforms and marketplaces. Document full transaction details from each channel – whether the sale comes from your online store, Amazon, eBay, or other marketplaces. Then, track gross and net sales separately.

Gross sales reflect the original product price before any reductions. Net sales show actual revenue after discounts, refunds, and chargebacks.

Make sure to record discounts, refunds, and chargebacks separately as contra-revenue entries. This prevents inflating your actual sales performance and gives you a clearer picture of how much revenue each channel actually generates.

For example, a customer buys a $100 shirt using a $10 discount code. Your books should record $100 in gross sales and a separate $10 discount entry.

Marketplace fees and payment processor charges should also be tracked independently, rather than netted against revenue, to provide a clearer picture of sales performance and operating costs across each channel.

Step 2: Tracking ecommerce expenses

Once you’ve captured all sales data, the next challenge is understanding where that revenue actually goes, which makes expense tracking the critical second step.

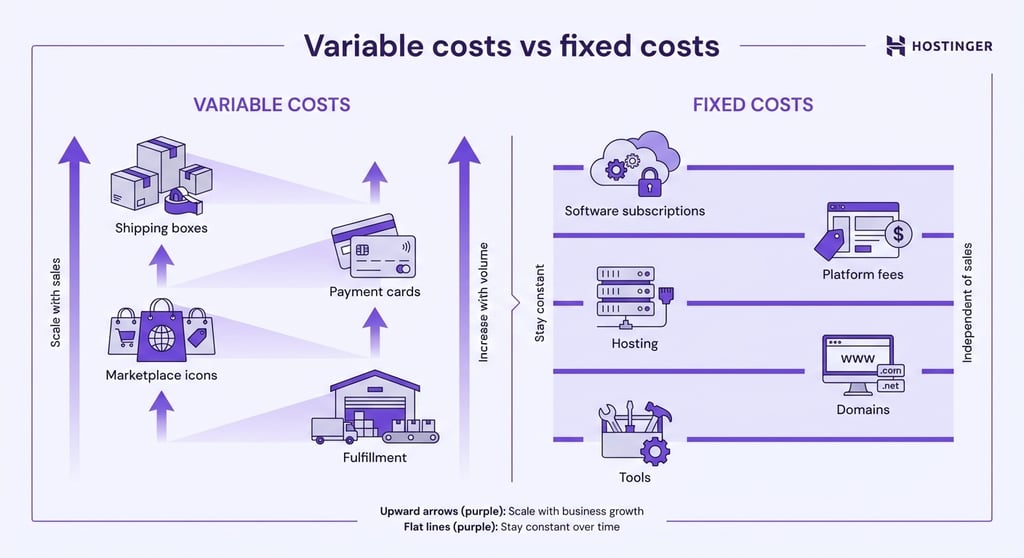

Ecommerce expenses typically fall into two categories: variable costs, which fluctuate with sales volume, and fixed costs, which remain relatively stable month to month.

Variable costs include expenses tied directly to each sale, such as shipping and packaging materials, payment processing fees, marketplace referral fees, and transaction-based fulfillment costs.

As sales increase, these expenses rise as well. For example, if you process 100 orders with $2.50 in shipping costs per transaction, that’s $250. Double your orders to 200, and shipping costs rise to $500. Tracking these costs accurately helps you understand your true cost per order.

Fixed costs are recurring expenses that don’t change based on sales activity. These include software subscriptions, ecommerce platform fees, hosting, domains, and core business tools like email marketing platforms.

No matter if you sell 100 or 1,000 products in a month, these costs remain the same. But they still need to be accounted for to avoid overstating profits.

By consistently categorizing ecommerce expenses, you gain a clearer view of your overhead, protect the accuracy of your financial reports, and make better decisions about pricing, marketing spend, and growth.

Step 3: Reconciling payments and payouts

While recording sales and expenses tells you what should happen financially, reconciliation confirms what actually happened.

Compare sales, fees, refunds, and payouts recorded in your books against reports from payment processors, ecommerce platforms, and bank statements.

This is often the most challenging part of ecommerce bookkeeping due to timing differences.

Payment processors don’t always deposit funds immediately, as some payouts take several days to settle. Others include rolling reserves, where processors temporarily hold a percentage of your revenue to cover potential chargebacks or disputes.

Stripe, for example, may hold 1-5% of revenue for 90 days for high-risk merchants.

Reconciliation ensures that amounts marked as “pending” in your ecommerce or payment apps eventually match the “available” funds deposited in your bank.

By reconciling regularly, you can confirm that all payouts are received, fees are correctly deducted, and no transactions are missing – keeping your books accurate and your cash flow visible.

Step 4: Managing inventory and COGS

The fourth step is tracking inventory accurately so you can calculate your cost of goods sold (COGS) correctly.

Inventory represents money you’ve spent on products that haven’t sold yet, which is why it appears on your balance sheet as an asset rather than an expense.

COGS only includes the direct cost of the products you actually sell during a given period.

For example, if you purchase 1,000 products at $5 each, the full $5,000 remains recorded as inventory. Each time one unit is sold, $5 is moved from inventory to COGS, reflecting the actual cost of that sale.

Ecommerce businesses typically use inventory valuation methods such as first-in, first-out (FIFO) or weighted average cost to determine which inventory costs are assigned to each sale.

With FIFO, you assume the oldest inventory sells first. For example, you purchase 100 units at $5 in January, then 100 units at $6 in February.

When you sell 150 units in March, COGS includes all 100 January units ($500) plus 50 February units ($300), totaling $800. The remaining 50 units stay in inventory at $6 each ($300).

Consistent inventory tracking ensures COGS is reported accurately, margins aren’t overstated, and financial reports reflect your products’ actual profitability.

Step 5: Generating financial reports

Finally, the ecommerce bookkeeping process culminates in financial reports.

With accurate sales, expense, payment, and inventory data in place, you can generate the financial reports that transform this information into business insights:

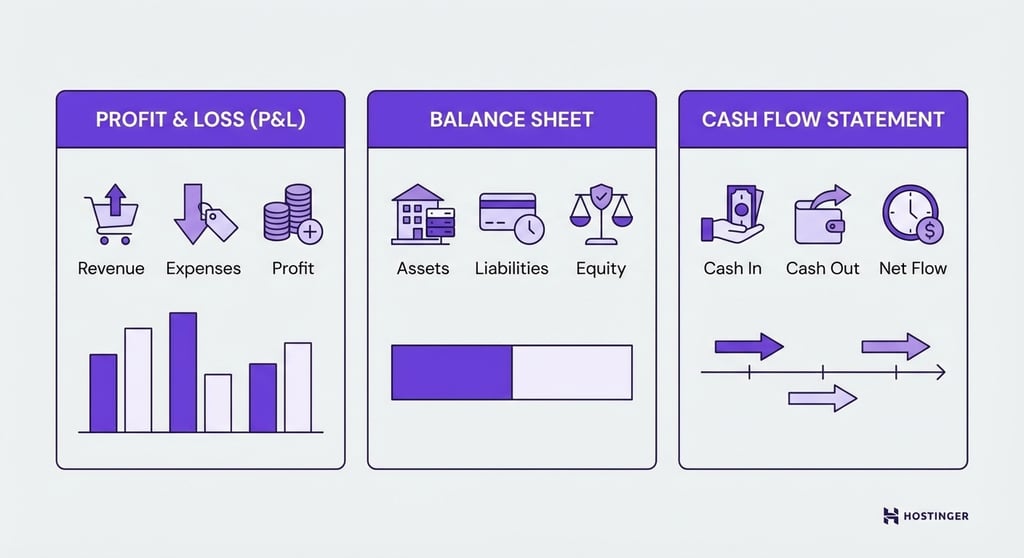

- The Profit and Loss (P&L) statement summarizes your revenue, expenses, and COGS over a specific period to show whether your online store is operating at a profit.

- The Balance Sheet provides a snapshot of what your business owns and owes, including cash, inventory, and liabilities.

- The Cash Flow Statement is especially critical for online store bookkeeping, as it tracks when cash actually moves in and out of the business, helping you manage timing gaps caused by settlement delays and payout schedules.

Together, these reports turn raw bookkeeping data into financial clarity, allowing you to monitor performance, plan ahead, and avoid cash flow surprises.

Simplify bookkeeping with Hostinger Website Builder

Reconciling sales across multiple platforms creates most ecommerce bookkeeping headaches. Hostinger Website Builder eliminates this by centralizing your store operations in one dashboard.

With zero transaction fees, you avoid the complex fee structures that make expense categorization difficult. This means fewer line items to reconcile and clearer profit margins.

The built-in data export capabilities also let you push clean sales data directly into third-party bookkeeping software – reducing manual entry and the errors that come with it. For stores processing 100+ orders monthly, this automation saves 3-5 hours of reconciliation work each week.

What are the key tasks in online store bookkeeping?

Managing an online business requires ecommerce bookkeeping tasks that go beyond traditional brick-and-mortar bookkeeping.

As ecommerce transactions occur across multiple platforms and payment systems, these tasks must be performed consistently to ensure financial data remains accurate and reliable.

The frequency of each task directly affects the trustworthiness of your reports and the speed at which you can spot issues.

1. Sales channel tracking

One of the most essential ecommerce bookkeeping tasks is tracking revenue across all sales channels where your products are listed. This may include your own ecommerce site as well as marketplaces like Amazon, eBay, or Etsy.

As each platform uses different reporting formats, payout schedules, and fee structures, manual tracking can be difficult and time-consuming.

To maintain accuracy, sales data from each channel should be reviewed regularly and consolidated into a single system.

Using tools that aggregate this data helps ensure you’re seeing a complete picture of your daily revenue without having to log into multiple dashboards or miss marketplace-specific adjustments.

2. Expense categorization and tracking

Accurate ecommerce expense tracking involves labeling every outgoing transaction so it can be analyzed, reported, and used for tax purposes. Proper categorization allows you to understand spending patterns, control costs, and calculate true profitability.

Common ecommerce expense categories include:

- Advertising, including Google Ads, Facebook Ads, and influencer partnerships

- Merchant fees, including credit card and payment processor fees

- Packaging and shipping supplies, including boxes, tape, labels, and branded inserts

- Software and tools, including ecommerce platforms, email marketing apps, and SEO tools

Consistently categorizing expenses reduces errors and ensures financial reports reflect real operating costs.

3. Tax-related bookkeeping tasks

Sales tax bookkeeping is one of the most complex responsibilities for ecommerce businesses. Online sellers must track customers’ locations and determine whether they have sales tax nexus – a significant presence in a state that requires tax collection.

Nexus is typically established through physical presence, like offices, warehouses, or employees in a state, or by exceeding economic thresholds. Most states establish nexus when annual sales exceed $100,000, though specific thresholds and rules vary by state.

Bookkeeping supports tax compliance by maintaining detailed records of taxable sales, collected tax amounts, and supporting documentation. Accurate, up-to-date records make it easier to file returns, respond to audits, and avoid penalties caused by under-collection or reporting errors.

What are the best ecommerce bookkeeping tools?

Below are some of the best ecommerce bookkeeping tools that can handle both bookkeeping and accounting tasks:

- QuickBooks Online. Cloud-based bookkeeping software for ecommerce that handles invoicing, expense tracking, sales reconciliation, and financial reporting. It integrates with major online stores and marketplaces. You can also use the Plus plan to add built-in inventory management tools.

- Xero. A popular ecommerce accounting software known for its cloud-based ease of use, multi-currency support, bank feeds, and seamless integration with ecommerce platforms. It’s ideal for small to mid-sized online sellers who want real-time bookkeeping and reporting.

- Zoho Books. A comprehensive ecommerce accounting and bookkeeping software that simplifies financial management with invoicing, expenses, bank reconciliation, and basic inventory features. Its automation helps reduce manual work for growing ecommerce stores.

- Wave. Free bookkeeping software for ecommerce and small businesses that covers core functions like income and expense tracking, bank reconciliation, and basic reports. It’s a good starter option for merchants on a tight budget before upgrading to more advanced systems.

- A2X. Not a full accounting system on its own, but a powerful ecommerce bookkeeping tool that integrates with systems like QuickBooks or Xero to automate marketplace payouts, fees, taxes, and settlement reconciliation.

💡 Pro tip: Social commerce sales are expected to reach $8.5 trillion by 2030, making it a significant revenue channel to grow your online store. So, if you plan to sell online across platforms like Instagram, TikTok, and Facebook, make sure your bookkeeping systems can consolidate sales data from these channels alongside traditional marketplaces.

Ecommerce bookkeeping costs

Ecommerce bookkeeping costs vary depending on your store’s size, order volume, and operational complexity. Expenses will increase as transactions and sales channels grow.

Typically, these costs fall into two categories: software subscriptions and bookkeeping labor, whether handled in-house or outsourced.

Software and tools costs

Most ecommerce businesses rely on a mix of bookkeeping, ecommerce accounting software, and other tools to automate data capture, reconciliation, and reporting. Costs vary depending on features, users, and integration capabilities:

- Bookkeeping and accounting software. Core bookkeeping systems typically cost $15-30/month for basic plans, which cover income and expense tracking, bank feeds, and standard reports. More advanced tiers, with features like multi-currency support, automation rules, inventory tracking, or advanced reporting, often range from $50-100+/month. Add-ons such as payroll or project tracking can further increase the monthly cost.

- Integrations. Connecting your accounting software to ecommerce platforms, payment gateways, or POS systems often requires paid integration tools. These typically range from $10-100+/month/integration, depending on order volume, the number of sales channels, and the level of automations. While these tools reduce manual reconciliation and errors, they increase overall ecommerce bookkeeping costs.

Labor and professional service costs

In addition to software, most ecommerce businesses incur labor costs to keep their books accurate and up to date. These costs vary depending on whether bookkeeping is handled in-house or outsourced, as well as your store’s size and complexity.

- In-house bookkeeping. Hiring a full-time bookkeeper involves covering salary, benefits, and ongoing training. In the US, an in-house bookkeeper typically costs $40,000-65,000 yearly, not including benefits. For smaller ecommerce stores, this can be expensive relative to the workload. However, for larger businesses with high order volume, multiple sales channels, or complex inventory, an in-house specialist may be justified for day-to-day financial oversight.

- Freelance bookkeepers. Outsourcing your bookkeeping needs using freelance services is a cost-effective option for growing ecommerce stores. They usually charge an hourly rate of $25-75 or offer monthly retainers ranging from $200-600, depending on transaction volume and reporting needs. Freelancers are well-suited for single-channel stores or businesses that need basic reconciliation and monthly reports without advanced analysis.

- Bookkeeping agencies or ecommerce accounting services. Bookkeeping firms and ecommerce-focused accounting services typically charge more but provide broader expertise and structured processes. Monthly fees range from $500-2,000+, depending on order volume, number of sales channels, inventory complexity, and tax requirements. These services commonly include reconciliation, financial statements, and tax-ready reports, making them a strong option for growing or multi-channel ecommerce businesses.

Cost of bookkeeping errors

Errors in ecommerce bookkeeping often cost far more than doing things correctly in the first place. Inaccurate or inconsistent records can lead to tax issues, flawed decision-making, and cash flow problems that directly affect your business’s sustainability.

One of the biggest risks is tax exposure. Missing transactions, misclassified expenses, or incorrect sales tax records can trigger penalties, interest charges, or audits.

When documentation is incomplete, fixing the problem often requires time-consuming rework or the help of professionals, adding unexpected costs on top of the original mistake.

This is where businesses often realize that underestimating bookkeeping software costs or delaying professional help can be more expensive in the long run.

Poor bookkeeping also leads to bad financial decisions. If your numbers are inaccurate, you may think a product is profitable when it’s not, overspend on advertising, or price products without accounting for rising costs. This directly impacts your ecommerce profit margins, making it harder to grow or even stay afloat.

Cash flow issues are another common consequence. Without reliable reconciliation and reporting, businesses may overestimate available cash while funds are still tied up in platform settlement delays or reserves. This can result in missed payments, stalled inventory purchases, or reliance on short-term financing.

In many cases, businesses turn to ecommerce bookkeeping services only after problems arise. While cleanup and correction are possible, they are often more expensive than ongoing, proactive bookkeeping.

For growing stores, investing early in accurate systems or considering outsourced bookkeeping helps prevent costly errors and provides financial clarity as the business scales.

Best practices for ecommerce bookkeeping

Following proven bookkeeping habits helps ecommerce businesses maintain financial accuracy, reduce errors, and make better decisions as they scale. These best practices are essential for online sellers managing multiple platforms, payment processors, and frequent transactions.

- Separate personal and business finances. One essential online store bookkeeping tip is to keep personal and business finances completely separate. Use a dedicated business bank account and credit card to ensure clean records, simplify tax reporting, and avoid confusion when reviewing financial statements.

- Automate data collection wherever possible. Bookkeeping automation reduces manual data entry and minimizes human error. Connect your ecommerce platform, payment processors, and bank accounts directly to your bookkeeping software so sales, fees, and payouts flow into one system automatically.

- Reconcile accounts on a regular schedule. Don’t wait until month-end or tax season to reconcile your books. Weekly or biweekly reconciliation helps catch missing deposits, duplicated transactions, and timing differences before they become costly problems.

- Document everything consistently. Keep digital copies of invoices, receipts, and contracts tied to each transaction. Clear documentation supports tax filings, simplifies audits, and makes it easier to explain discrepancies if questions arise later.

- Review financial reports frequently. Regularly reviewing your profit and loss statement, balance sheet, and cash flow report ensures your numbers remain accurate and actionable. Consistent reviews help you spot rising costs, declining margins, or cash flow gaps early.

- Standardize expense categories and rules. Use consistent income and expense categories across all tools and team members. Standardization improves reporting accuracy and makes trends easier to analyze over time.

When applied consistently, these habits turn bookkeeping from a reactive task into a proactive tool for managing and growing an ecommerce business.

All of the tutorial content on this website is subject to Hostinger's rigorous editorial standards and values.

Larassatti Dharma is a content writer with 4+ years of experience in the web hosting industry. She has populated the internet with over 100 YouTube scripts and articles around web hosting, digital marketing, and email marketing. When she's not writing, Laras enjoys solo traveling around the globe or trying new recipes in her kitchen. Follow her on LinkedIn

Comments

0 responses